Officials from the Federal Reserve indicated during their most recent meeting that they might encounter “difficult trade-offs” in the upcoming months, with rising inflation occurring alongside increasing unemployment. This perspective was supported by projections from Fed staff that highlighted heightened risks of a recession, as revealed in the newly released Minutes from the May 6-7 session.

In addition, central bank policymakers are faced with a dilemma regarding the rising inflation and unemployment. They must choose between implementing tighter monetary policy to combat inflation or reducing interest rates to foster growth and employment.

Key Quotes

- Participants at the Fed’s May 6–7 meeting agreed they were well positioned to wait for more clarity on the outlook.

- Participants agreed that risks of higher inflation and higher unemployment had risen.

- Participants agreed that uncertainty about the outlook had increased and it was appropriate to take a cautious approach to monetary policy.

- Almost all participants commented on the risk that inflation could prove more persistent than expected.

- Participants noted they may face ‘difficult trade-offs’ if inflation proved more persistent while outlooks for growth and employment weakened.

- Participants saw uncertainty about their economic outlooks as unusually elevated.

- Staff projection for 2025 and 2026 GDP growth was weaker than their estimate at the March meeting.

- Staff cited tariff policies as implying a larger drag on activity than policies they had assumed in their prior forecast.

- Committee voted to renew Dollar and foreign currency swap lines.

- These participants noted that a durable shift in such correlations or a diminution of the perceived safe-haven status of US assets could have lasting implications for the economy.

- Some participants commented on changes in typical correlations across asset prices in the first half of April.

Market reaction

The Greenback keeps its bullish stance in the wake of the FOMC Minutes, with the US Dollar Index (DXY) hovering just below the psychological 100.00 hurdle amid a small rebound in US yields across the curve.

This section below was published as a preview of the FOMC Minutes of the May 6-7 meeting at 13:15 GMT.

- The Minutes of the Fed’s May 6-7 gathering are due on Wednesday.

- The Federal Reserve kept the benchmark interest rate on hold, as expected.

- The US Dollar is at risk of piercing its 2025 low amid tariff-related concerns.

The Federal Open Market Committee (FOMC) will release the Minutes of its May 6-7 meeting on Wednesday. Back then, policymakers decided to keep the Fed Funds Target Range (FFTR) unchanged at 4.25%-4.50%, as widely anticipated by market participants.

The Federal Reserve (Fed) adopted a more hawkish stance at the beginning of the year, amid concerns about United States (US) President Donald Trump’s tariffs’ potential impact on economic progress and inflation.

Not only did officials decide to keep the benchmark interest rate on hold, but they also gave no hints on future rate cuts, maintaining the wait-and-see stance adopted in March.

The Fed is concerned about risks lying ahead

Fed officials noted, “Uncertainty around the economic outlook has increased. The Committee is attentive to the risks to both sides of its dual mandate,” according to the statement released alongside the decision.

Later in the press conference, Chairman Jerome Powell stated, “We are comfortable with our policy stance.” “We think that right now, the appropriate thing to do is to wait and see how things evolve. There’s so much uncertainty,” he added.

Additionally, the Fed slowed the pace of decline of its securities holdings. The central bank has been allowing up to $25 billion in Treasuries to mature every month, and reduced the roll-off to just $5 billion starting in April. Shrinking the balance sheet is another tool the Fed uses to control inflationary pressures.

President Trump’s massive tariffs have been the main reason behind the latest Fed’s hawkish stance. Despite his usual caution, Chairman Powell finally acknowledged that tariffs are “a good part” of their increased expectations for higher inflation. He added it would be “very difficult” to assess how much of the inflation is coming from tariffs.

“Looking ahead, the new Administration is in the process of implementing significant policy changes in four distinct areas: trade, immigration, fiscal policy, and regulation. It is the net effect of these policy changes that will matter for the economy and for the path of monetary policy,” Powell said.

When will FOMC Minutes be released and how could it affect the US Dollar?

The FOMC is set to release the Minutes from its May 6-7 policy meeting at 18:00 GMT on Wednesday, and market players hope the document will shed some light on the future of monetary policy.

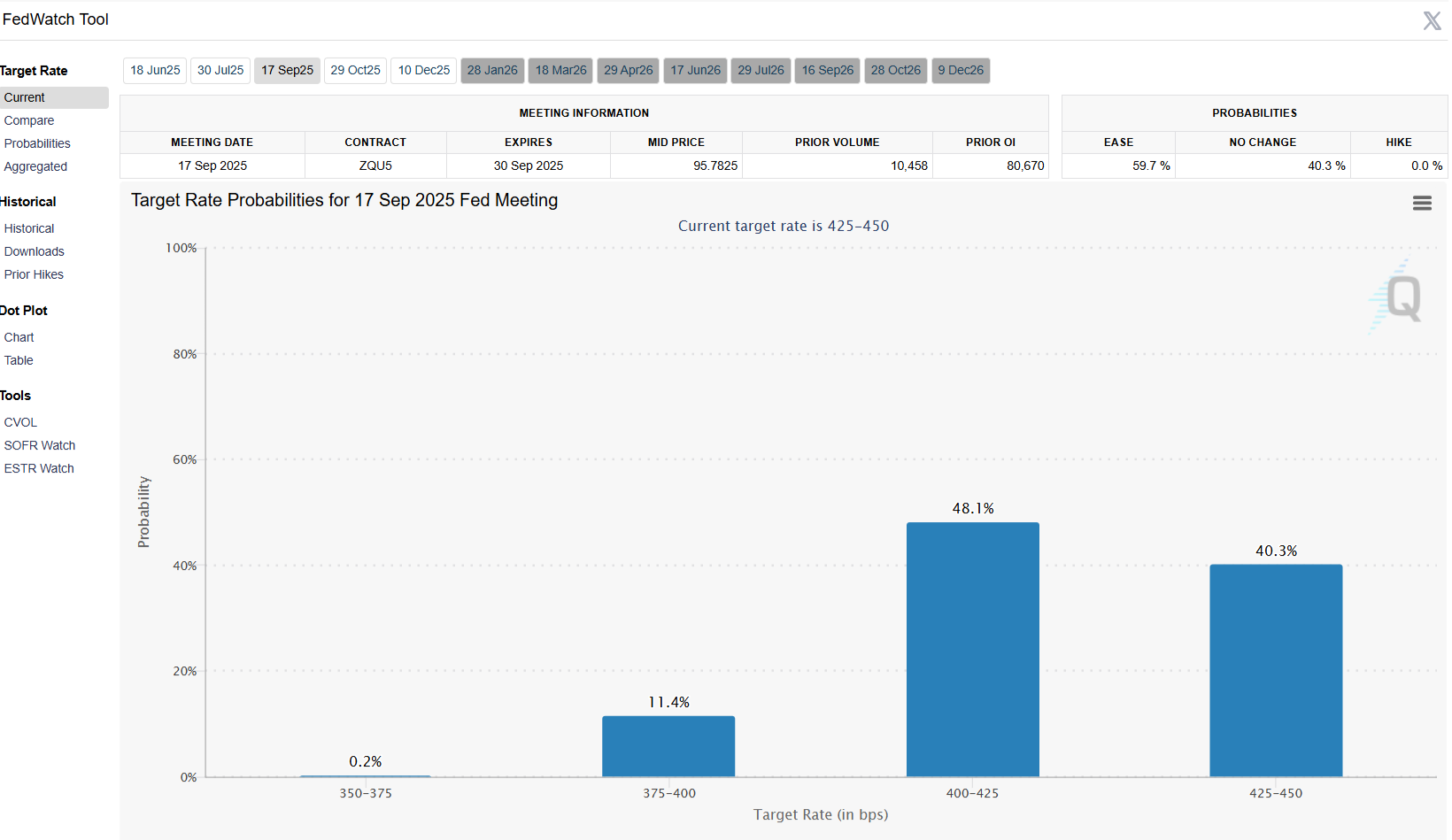

Ahead of the release, the CME FedWatch Tool shows speculative interest does not expect interest rate cuts in June or July, with the odds for a 25 basis-point (bps) cut standing at around 48% in September.

The US Dollar is under selling pressure ahead of the event, with the US Dollar Index (DXY) comfortably below the 100.00 mark. The Fed is not expected to adopt a dovish stance, meaning that most of what they could reveal is aligned with what the market already knows. The FOMC Minutes should then have a limited impact on the DXY.

Valeria Bednarik, Chief Analyst at FXStreet, says: “The DXY trades not far above the multi-month bottom posted in April at 97.91, and the risk skews to the downside, according to technical readings in the daily chart. The index develops below all its moving averages, with a flat 20 Simple Moving Average (SMA) providing resistance at around 100.20. Gains beyond the latter expose the 101.00 area, ahead of the May peak at 101.98. Still, such an advance seems out of the picture, given limited buying interest. Technical indicators in the mentioned time frame advanced, but remain well below their midlines, falling short of supporting a steady advance.”

Bednarik adds: “On the other hand, relevant support comes at 98.70, May monthly low. A bearish breakout exposes the mentioned April low, followed by the 97.50 region.”

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.